Treasury Secretary Yellen does not see any indicator of an imminent recession.

She isn’t looking. The normal economic tailwinds have calmed and, as predicted, Biden's economic policies are a significant headwind.

A recession is sometimes defined

as a reduction in the number employed nationally for a couple of months. Other times it is defined as a reduction in real

GDP for two quarters or more.

When it comes to predicting

events like this, my recursive approach is to first understand where the

general trends are heading. In technical

terms, is the economy’s “steady state” above or below where we are now, and how

much? If the trends are strong up, small

perturbations around that trend will not make a recession. If the trends are flat, then even a small negative

shock will create a recession by one or more of the definitions. Which definition will be triggered can be

assessed by contrasting employment trends with productivity trends.

Four important trends are worth

considering: organic productivity growth, organic population growth, recovery

from the pandemic recession, and new public policies affecting productivity, population,

or employment.

Organic trends

Given that recessions are defined

in absolute rather than per capita terms, population growth is normally an

economic tailwind. However, annual adult

population has fallen from a bit above one percent 1980-2018 to about 0.4

percent. Illegal immigration is a wild

card here because we do not know how many are immigrating, what fraction are adults,

and whether and how those adults will be economically engaged. With that caveat, we now are in a situation

where even a small negative shock that would not have caused a recession in the

one-percent population growth era will now.

Recovery from the pandemic was

also a tailwind. It someday will

continue to lift employment, but at the moment it

looks like employment has recovered as much as it can given

the serious health problems encountered during the pandemic, including but not

limited to self-destructive substance abuse habits that are not complementary

with productive employment. Some of

these people will show up on payrolls but how reliably they show up for work is

another question. Diabetes, liver

disease and heart disease have gotten out of control since 2020.

Workers lost skills and capital

laid idle during the pandemic. These are

recovering, although their recovery will not be fully recognized in the growth

data. GDP and productivity levels were

exaggerated during the pandemic as many goods were unavailable or low quality

in ways not captured by the national accountants. For example, public school teachers stayed

home from school but the national accountants assumed

that they were as productive as ever merely because they continued to get

paid. As they get back to traditional

teaching, this will not be officially recognized as economic progress for the

same reason the pandemic regress was never acknowledged.

Crime has gotten bad, especially

in big cities where productivity is normally the highest. Consumers and businesses are avoiding big cities,

which is a cost (“excess burden”) beyond the crime statistics because the whole

point of the avoidance behaviors is to keep from being one of those statistics.

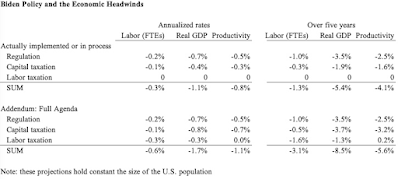

Fitzgerald, Hassett,

and I predicted

in 2020 that Biden’s economic agenda would reduce the levels of full-time

equivalent employment per capita by 3.1 percent and real gdp

per capita by 8.5 percent. If that level

effect were spread over five years, that would be 0.6 percent per year and 1.7

percent per year, respectively, as shown in the Table as an addendum panel. That by itself makes a recession likely in

one of those five years.

Regulatory Policy

Our analysis of Biden’s agenda distinguished

regulation from capital taxation from labor taxation. His regulatory agenda seems to be going ahead

as we expected. The good news is that Biden’s

nomination of David Weil to the Department of Labor was rejected

by the Senate and Biden was slow to fully mismanage the National Labor

Relations Board. But we did not anticipate

that Biden’s DOL would disrupt labor markets as much as it did with its mask

mandates. Sticking

with our original estimate, it looks that Biden’s regulatory agenda is

reducing employment by 0.2 percent per year (of five years) and real GDP by 0.7

percent per year below the organic trends.

See the Table’s top panel.

Of particular concern over the

next few months is the reliability of the

electric grid and air

travel. Snafus of this type are

already built into our regulatory analysis but these examples put more texture

on the economic reasoning that links the marginal regulations with poor

economic performance.

Capital Taxation: Inflation Sneaks

In

Biden’s Build Back Better bill

would implement much of the capital taxation we envisioned in 2020. The good news is that the bill has not yet

passed, and passage of its capital tax elements are not imminent in some other

form. The bad news is that inflation is

taxing businesses without any Congressional action (recall Feldstein

and more

recently Hassett on the effect of inflation on

the cost of capital), while it appears that Biden will let temporary provisions

in the 2017 TCJA expire. With capital

taxation during the Biden administration increasing about half of what we

expected, it would reduce real GDP by about 0.4 percent per year over five

years.

Speaking of inflation, higher Fed Funds rates are already showing up in mortgage rates. In effect, the Federal Reserve is introducing a tax (or cutting a subsidy) on structures investment, which is likely to send at least that sector into a recession. Socially responsible (a.k.a., woke) investing is also skewing the allocation of capital.

Combining capital taxation and

regulation, the headwinds in the Biden economy are 0.25 percent per year for

employment and 1.1 percent per year for real GDP.

Labor Taxation: Direction

Unclear

Labor taxation is an interesting

wild card here. Marginal tax rates on

work were cut sharply when the $300 weekly unemployment bonus expired last

summer. That effect has played out

already. But I expect that Congressional

Democrats, and even some Republicans, will expand unemployment benefits if

anything resembling a recession were occurring.

That could easily and quickly reduce employment by one percent, if not

more. On the other hand, various federal

health insurance subsidies are about to expire.

If they do (without resurrection), that will encourage work.

Bottom Line

Overall, a recession is highly likely

with so many headwinds and so few tailwinds.

A recession is more likely by the GDP definition than the employment

definition. The depth of the recession depends

on how much Congress destabilizes things by further adding to the already large

federal portfolio of programs for the unemployed and poor and further adding to

tax burdens.