Even if federal unemployment insurance expires at the end of the year, it will be replaced by an even more generous assistance program for people leaving their jobs.

Unemployment insurance is jointly administered and financed by federal and state governments, offering funds to “covered” people who lost their jobs and have as yet been unable to find and start a new one. The cash assistance comes weekly, with states paying benefits of about $300 a week for 26 weeks or until the person starts a new job, whichever comes first.

Normally, the assistance stops after 26 weeks, even if the beneficiary has yet to find a job. But during recessions the federal government’s temporary “extended” and “emergency” unemployment compensation programs pick up benefits after the state benefits are exhausted.

During the recent recession, the federal government paid benefits for up to 73 additional weeks, making the total benefit duration 99 weeks.

The temporary federal programs have expiration dates, but Congress has routinely extended them, at least through 2012. A couple of the federal programs fully expired that year, so in 2013 the unemployed could get benefits for no longer than 73 weeks.

The last remaining federal program, known as Emergency Unemployment Compensation, is set to fully expire at the end of this year. Congress has extended its final expiration date several times in the past – most recently as part of the fiscal cliff deal – but there is no guarantee that Congress will continue its extensions.

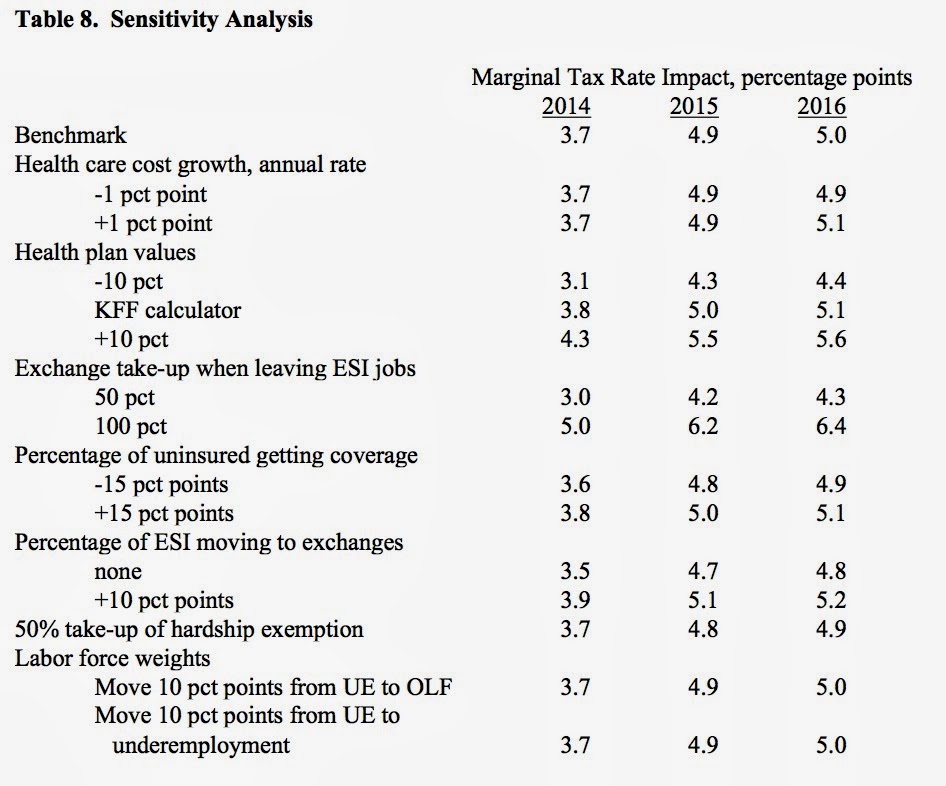

If the emergency program continues while the new health care assistance comes on line, the incentives of workers and employers to create and retain jobs will take a big hit. The solid line in the chart below shows my estimates of the average marginal tax rate on worker’s income, accounting for the fact that earning income on a job results in both additional taxes and withheld federal benefits. The higher the tax rate, the less is the incentive to work.

Casey B. Mulligan’s estimates of the impact of emergency unemployment compensation ending in December 2013.

Casey B. Mulligan’s estimates of the impact of emergency unemployment compensation ending in December 2013.The dashed line shows the marginal tax rate if the emergency program really does expire at the end of the year. Tax rates will increase in January, but much less than they would without the expiration, because the assistance lost from the emergency program will be offset by the health assistance coming online.

The federal unemployment benefits at risk of expiration are economically more important than the already-expired programs, because it is less common for unemployment to last more than 73 weeks (when the expired programs kicked in) than it is to last 26.

Unemployment benefits from any program help people who desperately need it, but they also keep the labor market depressed by permitting people to remain unemployed longer and making layoffs more common. The remaining emergency program is the most important and thereby does the most to help people and the most to keep the labor market depressed.

Even if the emergency program is allowed to expire on Jan. 1, it will ‘be replaced by an even larger program — the Affordable Care Act — assisting the unemployed and others, including premium subsidies for health insurance.

Most people have jobs that provide health insurance and will be ineligible for premium subsidies for as long as they work. But as soon as they are fired, quit, retire or otherwise leave the payroll, they will be eligible for monthly assistance to pay for their health insurance premiums and out-of-pocket expenses.

For households between 100 and 400 percent of the poverty line – that’s about half of households – the new assistance will average about $110 a week, tax free (unlike unemployment benefits, which are taxable). Moreover, the premium assistance is not limited to 26 weeks; it can last for decades.

Regardless of how you evaluate the relative costs and benefits of the emergency program, now is the time for Emergency Unemployment Compensation to expire to make way for new assistance programs.